Overview of the three Courses: subjects and teachers

(subject to change)

20 12 21a

A. Tax Treaty course

A.1. Key concepts of international tax law

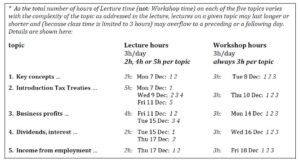

Mon 7* (lecture) & Tue 8 (workshop) December 2020

First, we will explore why and how countries tax cross-border income and the double taxation that will typically result therefrom (juridical and economic double taxation). Next, the various methods to relieve juridical double taxation will be examined: both their operation and their advantages & disadvantages. Finally, a brief overview is presented of the types of relief countries may offer regarding economic double taxation.

>> teachers: Prof. Kees van Raad (NL) (lecture) and Edgar Santos Gomes (Braz) & Daniel Cordeiro (Braz) (workshop)

A.2. Introduction to tax treaties and treaty residence

Wed 9* (lecture) & Thu 10 (workshop) December 2020

The interaction between the distributive articles and the double taxation relief provisions will be examined and explained, along with the key concepts of residence and source. ‘Residence’ will be further examined in some detail.

>> teachers: Prof. Kees van Raad (NL) (lecture) and Gustavo Carmona (Braz) (workshop)

A.3. Business profits taxation under tax treaties

Fri 11* (lecture) & Mon 14 (workshop) December 2020

The main topics of this comprehensive subject that will be visited include the contents and application of the distributive rules of OECD Model Article 7: the main rule and the exception if business is conducted through a `permanent establishment´ (PE) in the other state. Further, the concept of PE will be examined in some detail (physical PE, project PE, Agency PE; other non-OECD types of PE).

>> teachers: Prof. Kees van Raad (NL) (lecture) and Dalton Hirata (Braz) (workshop) & Eduardo Torretti (Chile) (workshop)

A.4. Dividends, interests & royalties and immovable property income & capital gains under tax treaties

Tue 15* (lecture) & Wed 16 (workshop) December 2020

The tax treaty rules on investment income vary with the nature of the investment. Immovable property income is typically subject to ordinary taxation in the source country whereas income from intangible rights (shares, debts, intellectual property rights) is usually subject to flat-rate gross-basis taxation in the source country with the residence country taxing it again with a tax credit provided for the source country tax. Taxation of investment income gives rise to numerous theoretical and practical issues the most important ones of which will be touched upon in this topic.

>> teachers: Prof. Kees van Raad (NL) (lecture) and Ana Carolina Monguilod (Braz) & Rodrigo Brunelli (Braz) (workshop)

A.5. Income from employment, pensions, etc. under tax treaties

Thu 17* (lecture) & Fri 18 (workshop) December 2020

The grown mobility of labor has greatly increased the importance of OECD Model Articles 15 through 20, each of which deals with a particular type of service income. The main rules are laid down in Article 15 which gives rise to a variety of important issues in international tax practice. In addition to an analysis of some of these issues, other points arising under the rules on the remuneration of directors, pensions, and the income of artistes and sportsmen will be discussed.

>> teachers: Prof. Kees van Raad (NL) (lecture) and Luis Henrique Costa (Braz) & Luciana Nóbrega (Braz) (workshop)

Click here for a list of short CVs and photos of the teachers

B. Advanced Subjects course

B.1. Tax treaty interpretation and application illustrated with complex cases from international tax practice

Mon 18 Jan 2021

The cases (based on personal practice of the teachers and on court decisions) will deal with a variety of issues that typically arise in the application of tax treaties, and that will deal inter alia with the points that are listed below. These cases will be used to discuss and analyze the general tax treaty rules that apply in those instances and will also cover some of the issues dealt with in the October 2015 (final) BEPS Action reports.

>> teachers: Prof. Kees van Raad (NL) & Edgar Ruiz (Colombia)

B.2. Taxation of technical services

Tue 19 Jan 2021

Brazil has a long history of including in its tax treaties a special provision (or expand the scope of the treaty article on royalties) in respect of fees for technical services. Since the 1990s, other developing countries in Asia, Africa and Latin America too have negotiated for including stand-alone clauses dealing with technical service fees in their tax treaties despite the absence of model clauses. The 2017 update of the UN Model included a new Art. 12A dealing with Technical Service Fees for the first time in recognition of tax treaty practices of countries such as Brazil. This class will focus on the genesis of art 12A of the 2017 UN Model, including the importance of each country’s domestic tax policy, the appropriate interpretive approach to the meaning of these clauses, potential overlap with other distributive rules, as well as the variety of restrictions that the different technical service income provisions in Brazil’s tax treaties impose on Brazil domestic rules.

>> teachers: Professor Johann Hattingh (South Africa), Edgar Gomes (Braz) & Ana Paula Saunders (Braz)

B.3. BEPS and the OECD/G20 Multilateral Instrument

Wed 20 Jan 2021

The final reports of the OECD/G20 BEPS project proposed many changes both to domestic tax law and tax treaties. The treaty changes comprise both compulsory minimum standards (Actions 6 and 14) and optional changes (Actions 2, 6 and 7). Pursuant to the Action 15 final report, the treaty changes are effected through the so-called Multilateral Instrument (MLI). Signatory countries will be able through this instrument to effectively amend their tax treaties with a single stroke. However, both the contents and the operational rules of the MLI are quite complex. This day’s class will explain how the procedural and substantive rules of the MLI operate. In addition it will be demonstrated how the original treaty text, after it has become subject to the overlay of the MLI changes and additions that result from the two treaty states having signed the MLI, must be interpreted and applied.

>> teacher: Prof. Kees van Raad (NL)

B.4. OECD Blueprint for Pillar One & Pillar Two

Thu 21 Jan 2021

In October 2019, the OECD’s CTPA Secretariat published for public discussion a 14-page `Unified Approach under Pillar One´ proposal for dealing with issues stemming from the digitization of the economy. It was followed up on 30 January 2020 by a 25-page Annex 1 to the Statement issued by the 137-member Inclusive Framework (this group includes Brazil). On 12 October 2020, the OECD’s CTPA and the Inclusive framework published discussion drafts (`Blueprints´) of the Report on Pillars 1 and 2 of the OECD approach to tax challenges arising from the digitalization of the economy. These comprehensive drafts will be analyzed and discussed in this class. it will also discuss the recent UN initiative for a new tax treaty provision (Art. 12B) dealing with certain types of digital transactions.

>> teacher: Dr Bruno da Silva (Port)

B.5. Brazilian CFC rules (Law 12,973/14)

Fri 22 Jan 2021

Law 12,973/14 has brought a new set of rules for the calculation of Brazilian taxes on foreign profits. This session shall discuss the main topics related to the new legislation and its interaction with OECD Model tax conventions.

>> teacher: Professor Sergio André Rocha (Braz)

B.6. Exchange of information

Mon 25 Jan 2021

The effectiveness of exchange of information under tax treaties (automatic, spontaneous or upon request) has greatly increased in the last two decades. In addition, the 1988/2010 OECD Convention on mutual administrative assistance in tax matters in which Brazil participates effectively since 2016, has a great impact on the amount of information received and sent by Brazil from and to other countries. Moreover, Brazil is a member of the Global Forum on Transparency and Exchange of Information for Tax Purposes in the area of the automatic exchange of information, in particular with respect to the Common Reporting Standard. All these initiatives have enabled Brazil to receive detailed information on foreign activities of Brazilian resident companies and individuals, permanently changing the former situation in Brazil.

>> teachers: Renata Fontana (Braz) & Ilka Marinho Pugsley (Braz)

B.7. Beneficial ownership and tax treaty anti-avoidance provisions

Tue 26 Jan 2021

The reduction of taxation of dividends, interest and royalties in the state of source is generally subject to the condition that the recipient of that income is the beneficial owner thereof. Although the term ‘beneficial owner’ was introduced in the OECD Model Convention in 1977, the interpretation of the term continues to give rise to difficulties. The background of the term and its interpretation in various countries will be the main topic of this lecture. In addition, other anti-avoidance provisions prevalent in tax treaties will be discussed in this lecture.

>> teachers: Vikram Chand (India)

B.8. Non-discrimination and double taxation relief under tax treaties

Wed 27 Jan 2021

The different non-discrimination clauses of Art. 24 of the OECD Model will be analyzed and compared with each other. We will discover how the non-discrimination provisions interact with the distributive rules and examine in which case taxpayers are in a similar situation. In the end we will discuss several triangular cases where non-discrimination issues will be combined with problems of double taxation relief (Art. 23 of the OECD Model). The discussion will include an analysis of the recent Volvo decision of the Brazilian Supreme Court.

>> teacher: Carolina Landim (Braz) & Chiara Bardini (Italy)

B.9. Cross-border investment: Brazil – Portugal – Angola (2 days)

Thu 28 & Fri 29 Jan 2021

There is a substantial volume of investment by Portuguese companies into Brazil. In the absence of a tax treaty between Angola and Brazil, most of the investment from Angola into Brazil is effected through a Portuguese resident entity making use of both the Angola-Portugal and the Portugal-Brazil tax treaties. Also from Brazil there is investment in Portugal and in Angola (through the Brazil-Portugal and Portugal-Angola tax treaties).

This topic of the Advanced Subjects course focuses on the particular issues that may arise, taking into account features of the domestic law of the three countries, and will discuss approaches to take and solutions to consider.

In addition, with regard of Brazilian and Angolan companies investing in member states of the European Union, a brief overview is presented of the particular aspects of EU tax law that are important for investors resident in third-countries that invest in an EU Member state (including but not limited to Portugal).

>> teachers: Dinis Tracana (Port), José Guerra (Port) & Rafael Dinoá (Braz)

Click here for a list of short CVs and photos of the teachers

C. Transfer Pricing course

This course will be taught primarily from the perspective of the OECD Transfer Pricing Guidelines (TPG) by teachers from overseas, in view of the likely scenario that Brazil will move in the next few years to these TPG. During the last 20-30 minutes of each class a Brazilian teacher will highlight the current Brazilian perspective on the issues discussed.

C.1. Introduction to TP

Mon 1 Feb 2021

The arm’s length principle is the international standard set by the OECD to determine the transfer prices in intragroup situations. In the last decade, the new organizational models adopted by MNEs and the different kind of transactions arising led the OECD to launch new projects in order to fine-tune the 1995 Guidelines with the current economic scenario. This class will firstly focus on the milestones of the arm’s length principle, its recent developments, and why it is still, as confirmed by the OECD report on Base Erosion and Profit Shifting, a hot topic for MNEs.

>> teacher: Dinis Tracana (Port) & Alexandre Siciliano (Brazilian aspects)

C.2. Comparability analysis

Tue 2 Feb 2021

This class deals with the comparability analysis which represents a core element of transfer pricing and involves both the search for comparables (the so-called economic analysis) and the analysis of the taxpayer’s-controlled transaction. The course starts with an introduction to those elements of economics, accounting and statistics that provide the key knowledge for properly performing the comparability analysis. The focus of the course is on Chapter III of the OECD TP Guidelines. The standard practices applied by practitioners and tax authorities will be examined through an exploration of the theoretical framework and through case studies to be discussed with attendants of the course.

>> teacher: Dalton Hirata (Braz) & Igor Scarano (Brazilian aspects)

C.3. Transfer pricing methods (2 days)

Wed 3 & Thu 4 Feb 2021

The purpose of this lecture is to analyse the main features of the Transfer Pricing Methods outlined in the OECD TP Guidelines under both a theoretical and practical perspective. Case studies will be presented to address the main issues arising from the application of the different methods.

>> teacher: Mariana Martins Silva (Port) & Alexandre Siciliano and Igor Brandão (Brazilian aspects)

C.4. Intra-group services & Cost Contribution Arrangements (CCAs)

Fri 5 Feb 2021

Intra-group services are one of the issues that professionals are most often required to face nowadays in the transfer pricing field. Attendants will be provided with the tools required to understand whether an intra-group service has been provided and – in that case – whether it has been charged at an arm’s length price. In addition, the class will cover also the major topic of the Cost Contribution Agreements (CCA).

>> teacher: Leendert Verschoor (NL) & Luiz Felipe Centeno (Brazilian aspects)

C.5. Financial transactions

Mon 8 Feb 2021

The 2015 BEPS Action Plan reports on Action 4 (Limiting base erosion involving interest deductions and other financial payments) and Actions 8-10 (Aligning Transfer Pricing Outcomes with Value Creation) mandated follow- up work on the transfer pricing aspects of financial transactions. In particular, Action 4 of the BEPS Action Plan called for the development of `…transfer pricing guidance … regarding the pricing of related party financial transactions, including financial and performance guarantees, derivatives (including internal derivatives used in intra-bank dealings), and captive and other insurance arrangements.´ Under these mandates, the Committee on Fiscal Affairs produced the report ‘Transfer Pricing Guidance on Financial Transactions: Inclusive Framework on BEPS: Actions 4, 8-10’ in February 2020, which was included in the 2020 edition of the OECD TP Guidelines, in particular, the accurate delineation analysis under Chapter I, to financial transactions. It also provided guidance with specific issues relating to the pricing of loans, cash pooling, financial guarantees, and captive insurance. In this class, the main conclusions reached by the OECD will be outlined and explained through case studies to be presented to the attendants.

>> teacher: Patrícia Matos (Port) & Ramon Tomazela (Brazilian aspects)

C.6. Business restructurings and intangibles (2 days)

Tue 9 & Wed 10 Feb 2021

This class deals with the transfer pricing aspect of business restructurings which represents one of the most controversial issues in the transfer pricing arena due to its peculiarities (e.g., non recurrent transactions, use of evaluation techniques). Focus will be on Chapter IX of the OECD TP Guidelines. The standard practices applied by practitioners and the tax authorities will be examined through an analysis of the theoretical framework and through case studies in which real restructurings will be analyzed by addressing both the evaluation techniques used for determining the indemnification due and the way options realistically available should be identified.

>> teacher: Gábor Baranyai (Hungary) & Priscila Mariano (Brazilian aspects)

C.7. Digital economy

Thu 11 Feb 2021

This class will focus on the impact that the digitalization of the economy had on the business models of multinationals, leading to significant changes to their supply chains and value chains. Through case studies and practical examples, this class will outline the changes to the existing business models and address the transfer pricing issues arising therefrom.

>> teacher: Bhavita Kumar (India) & Victor Polizelli (Brazilian aspects)

C.8. Future challenges to TP

Fri 12 Feb 2021

In this class the discussion will revolve around the future challenges to TP and the trends that slowly start to develop. The class will address the impact of the Covid-19 pandemic in the business models of multinationals (as a result of the need for more local supply changes), in the evaluation of controlled transactions, trade between related parties and TP controversy. Other topics related to the growing connection between online networks (such as the Internet of Things) will also be briefly addressed.

>> teacher: Ligia Melo (Braz)

Click here for a list of short CVs and photos of the teachers